If approved by the lender, you take over the seller’s existing mortgage — including the interest rate, remaining balance, and time left on the loan.

For example: If the seller has 12 years left on their loan, you step in at year 12 — you don’t restart a new 30-year mortgage.

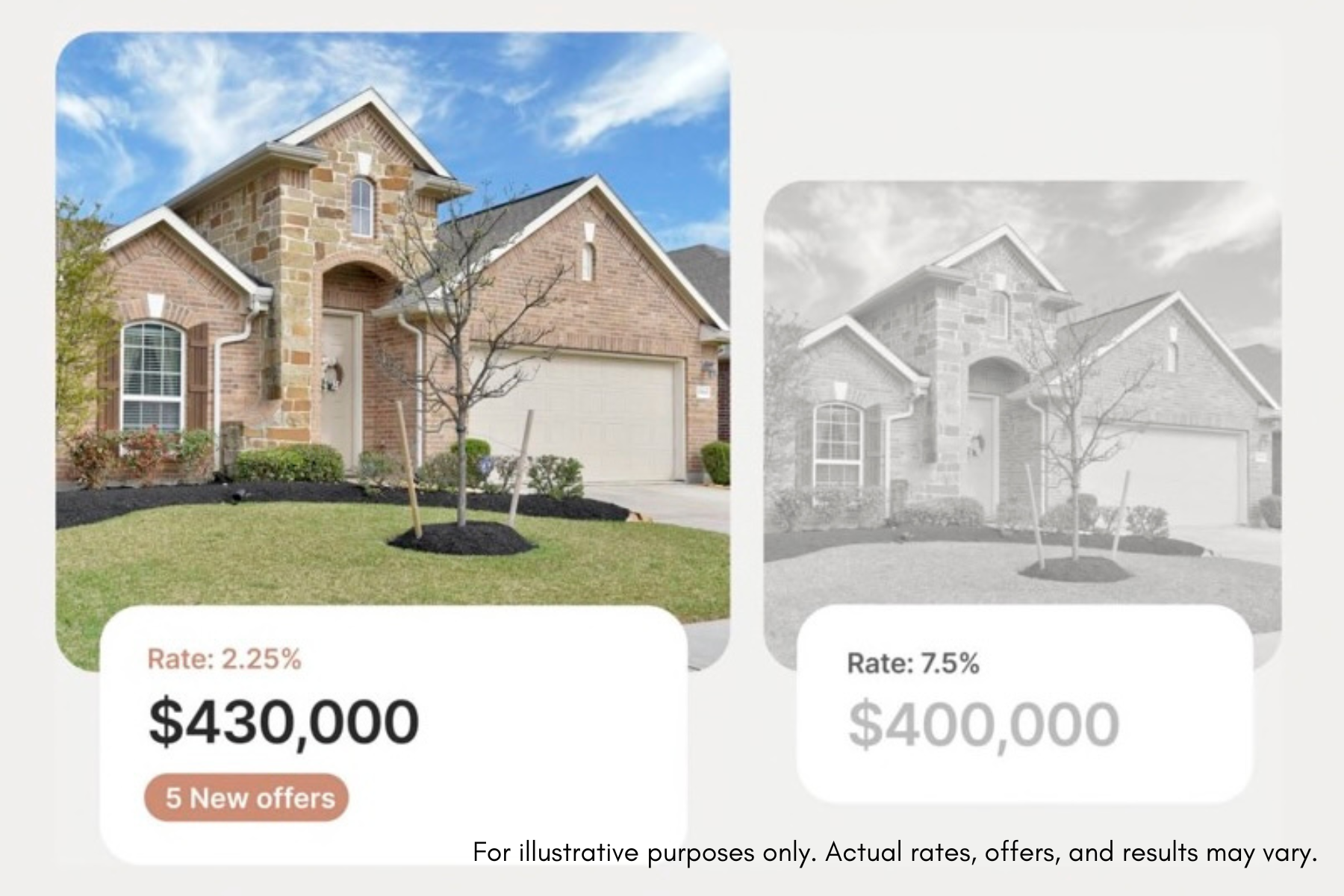

At closing, you bring cash to cover the seller’s equity, which is the difference between the purchase price and what’s still owed on the mortgage.

Because there’s no new loan being created, there’s no traditional down payment required. Your cash goes toward the seller’s equity instead — often allowing you to lock in a much lower rate than what’s available today.